0 comments

21 Feb , 2023

As unfavorable pricing continues, competitive market could weigh on workers’ comp

According to Fitch Ratings, workers’ compensation saw a combined ratio of 92% for the previous year. An immediate concern is the growing pressure from medical inflation, which had been somewhat tame in 2022. For the past year (ending Nov. 30, 2022), the medical consumer

0 comments

7 Feb , 2020

0 comments

29 Oct , 2019

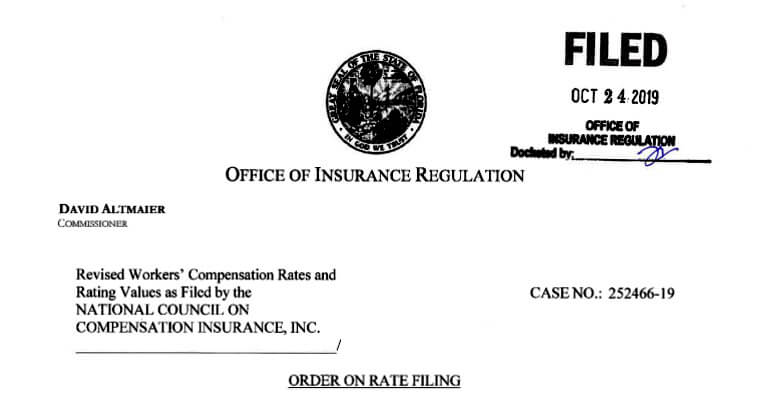

Florida Workers’ Comp Rates to drop 7.5 percent

Effective January 1, 2020, Florida Workers’ Comp Rates for new and renewal policies for other than the “F” classifications, the statewide overall rate level change shall be -7.5% for the filing. 1-866-684-5684 Contact us to have your Florida Workers’ Comp Rates verified. OIR Orders

0 comments

29 May , 2019

Fix diminishing agent commissions with Simple Work Comp

Do your commissions diminish upon renewal? If so, how big a hit will you take when your comp clients renew? 10%? 20%? 50%? As an agent you know all work comp carriers are not created equal. However, when it comes to agent commissions, some

0 comments

22 May , 2019

Placing your work comp clients with the state fund, is it worth it?

Do the commissions justify the paper work? How to get more reward from your hard-to-place work comp clients. Sometimes we all need to know when to cut our losses and move on. However, that’s easier said than done. As a work comp insurance agent,