by Matt C / on 19 December, 2023

Minimum Wage: Know Your Worth in the New Year

Employees are seeing this rise in most areas across the country!

But wait, isn't $7.25 the standard minimum wage? Nope! Across the United States, ...

by Matt C / on 21 February, 2023

As unfavorable pricing continues, competitive market could weigh on workers’ comp

According to Fitch Ratings, workers’ compensation saw a combined ratio of 92% for the previous year.

An immediate concern is the growing press

by Matt C / on 25 October, 2023

Will Climate Change The Home Insurance World?

The answer is yes, and at a rapid pace.

Home insurance prices are spiking across the US responding in part to the fallout from more frequent extre...

by Matt C / on 9 July, 2023

Through The Haze: Does Medical Cannabis Benefit Workers Compensation Claims?

Could the legalization of cannabis and psychedelics in workers' compensation complicate matters, or could it actually be a way to reduce costs? This ...

by Matt C / on 20 June, 2023

Can Small Business Employees Benefit From Using A PEO? The Answer Is… Yes!

As a small business owner, you're likely an expert in your field and have a passion for what you do. However, you probably didn't start your business...

by Matt C / on 1 June, 2023

Through The Haze: Does Medical Cannabis Impact Workers Compensation?

With insufficient research, this smoky area ends up causing more confusion than clarity, especially when it comes to its impact on work safety and ac...

by Matt C / on 14 January, 2023

Reduce Your Experience Modification Factor

There are three key factors that go into calculating a workers’ compensation (WC) premium:

The rate assigned to each payroll classification i

by admin / on 7 December, 2022

FINDING THE RIGHT PEO SERVICES

A business owner's guide to helping find the right PEO solution for their company. Download the FREE eBook today. When you are ready to make a decisi...

by admin / on 7 February, 2020

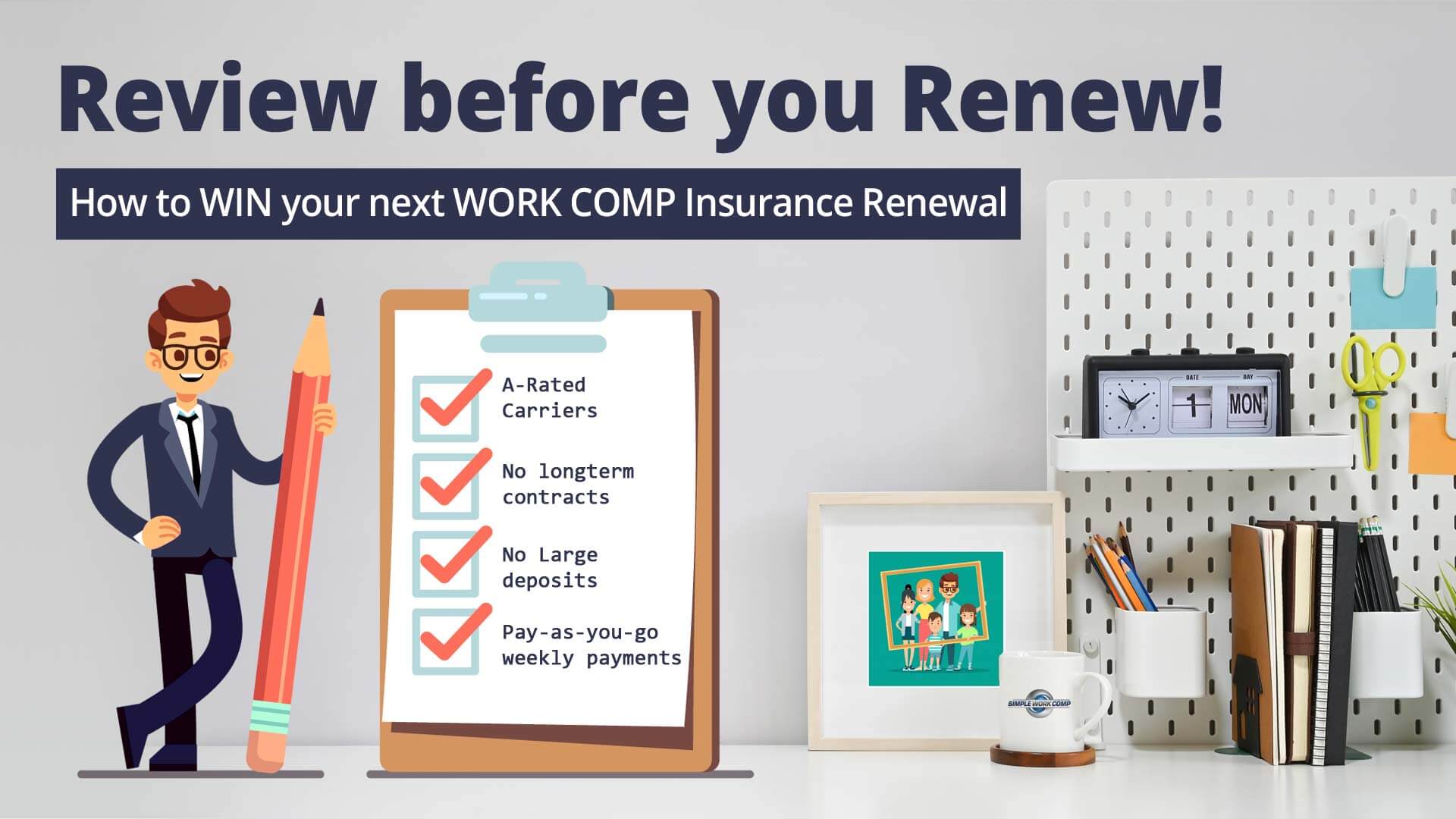

Review before you renew!

70% of work comp policy reviews result in lower premiums for our clients.

Need help now?Call us: 1-866-684-5684

The insurance ...

by admin / on 27 November, 2019

Small Business Saturday: One Business Owner to Another

Small Business Saturday is November 30th and if you are a small business owner, you obviously know about your customers and all about running you...